Lesson 3.1: The Importance of Saving

The Importance of Saving

Starting early isn’t just good advice — the numbers prove it’s worth hundreds of thousands of dollars.

By the end of this lesson, you’ll be able to:

- Explain four reasons saving is non-negotiable for financial health.

- Distinguish between an emergency fund, short-term savings, and long-term savings.

- Describe how compound interest turns time into money.

- Show why starting at 18 beats starting at 25 — even with less money put in.

- Name practical strategies for saving consistently without burning out.

1. Why Saving Actually Matters

Saving isn’t about being boring or depriving yourself. It’s about giving future-you options — the option to handle a crisis without panic, chase an opportunity when it shows up, and eventually stop trading time for money altogether.

A savings cushion means a blown tire or a medical bill is an inconvenience, not a disaster that sends you into debt.

Moving out, a car, travel, a business — none of it happens without money saved for it first.

Financial anxiety is one of the biggest stressors for young adults. A cushion doesn’t fix everything, but it changes the math on most crises.

Money sitting in a high-yield account or invested grows over time. Saved money becomes working money.

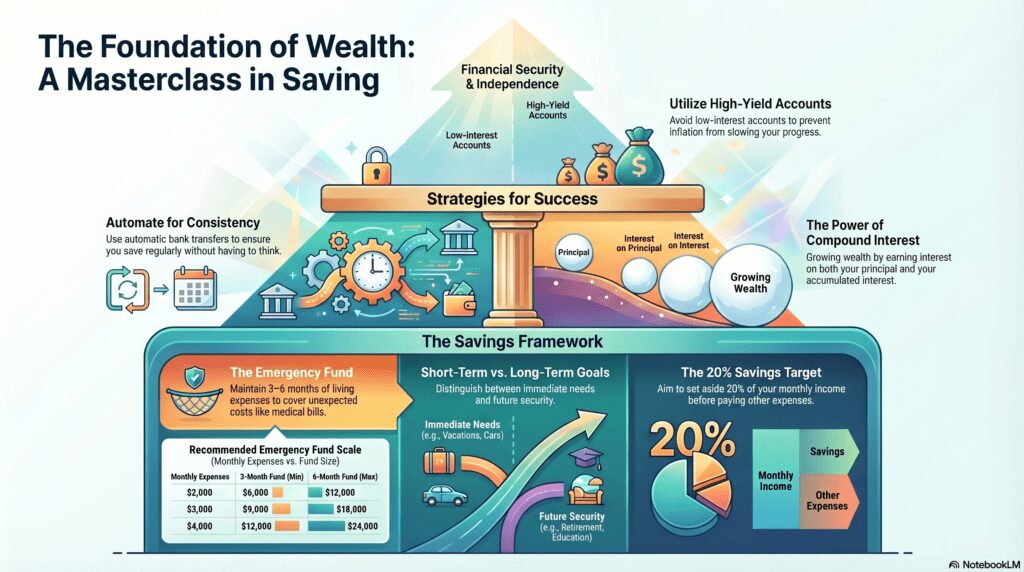

2. The Three Buckets of Savings

Not all savings have the same job. Think of them as three separate buckets, each with a different purpose and timeline.

Emergency Fund

Your financial seatbelt. Covers 3–6 months of living expenses for job loss, medical bills, or any surprise that can’t wait.

Short-Term Savings

Money earmarked for a specific goal within 1–3 years: a trip, a car, moving costs, or a new laptop.

Long-Term Savings

Money you won’t touch for 5+ years — retirement, a house down payment, building real wealth. This is where compound interest does its best work.

3. The Secret Weapon: Compound Interest

Compound interest means you earn interest on your balance — and then earn interest on that interest, and then on that, and so on. It snowballs. The longer it runs, the faster it grows. And the earlier you start, the more time it has to run.

Here’s the simplest way to see it: if you put $1,000 in an account earning 7% a year:

| Year | Balance | Interest earned that year |

|---|---|---|

| Year 1 | $1,070 | $70 |

| Year 5 | $1,403 | $92 |

| Year 10 | $1,967 | $129 |

| Year 20 | $3,870 | $253 |

| Year 30 | $7,612 | $498 |

Notice: by year 30, you’re earning more in one year ($498) than your entire original deposit ($1,000 × 49.8%). You put in nothing extra. Time did the work.

The cost of waiting — in real dollars

Same contribution: $200/month. Same hypothetical return: 7%/year. Same endpoint: age 65. Only the start date changes.

Starting at 18 vs. 25: ~$480,000 difference — for putting in only $17,000 more.

Starting at 18 vs. 35: ~$830,000 difference — for putting in only $41,000 more.

The gap isn’t about how much you contributed. It’s about how long compounding had to run. Time is the ingredient you can only get by starting now.

Illustration only, assuming a hypothetical 7% average annual return compounded monthly. Actual returns vary and are not guaranteed.

4. Where to Keep Your Savings

Not all savings accounts are equal. A regular checking or savings account at a big bank might pay 0.01% interest. A high-yield savings account (HYSA) at an online bank often pays 4–5% — sometimes more. Same FDIC protection, same access to your money, dramatically more interest earned.

Regular savings account (0.01%)

$5,000 saved earns about $0.50 in a year. That’s not a typo. Fifty cents.

High-yield savings account (~4.5%)

$5,000 saved earns about $225 in a year — just for keeping it in the right place. No extra effort required.

For your emergency fund and short-term savings, an HYSA is almost always the right move. For long-term savings, investing (covered in Lessons 3.2 and beyond) typically outperforms even the best savings account rates.

5. Saving Strategies That Actually Stick

Check Your Understanding

Pick your answer, then tap “Reveal answer” to check yourself.

1. How much should a fully stocked emergency fund ideally cover?

A) 1 month of expenses | B) 3–6 months of expenses | C) 1 year of income | D) Whatever’s left over after bills

Reveal answer & explanation

Correct: B. 3–6 months of living expenses gives you enough runway to handle job loss, a health issue, or a major repair without going into debt. A is too thin for most real emergencies. C is excessive for most people and ties up money that could be invested. D isn’t a real target.

2. What makes compound interest more powerful than simple interest?

A) It applies to a fixed amount every year. | B) You earn interest on your interest, so the balance grows faster over time | C) It’s only available in retirement accounts | D) Banks charge less for it

Reveal answer & explanation

Correct: B. With compound interest, every gain becomes part of the new principal, so future interest is calculated on a larger number. That snowball effect is what makes time so valuable. A describes simple interest. C and D are false.

3. Based on the comparison above, someone who starts saving $200/month at 18 ends up with roughly how much more than someone who starts at 25?

A) About $17,000 more | B) About $100,000 more | C) About $480,000 more | D) Roughly the same, since the monthly amount is identical

Reveal answer & explanation

Correct: C. Starting at 18 produces ~$1.07M vs. ~$591K starting at 25 — roughly a $480,000 gap. The person who started at 18 put in only $17,000 more out of pocket. The rest of the gap came from those extra 7 years of compounding. D is the most common misconception: the same monthly payment does not yield the same outcome when the time period differs.

4. Your check engine light just came on, and you need $600 for repairs. Which savings bucket should cover this?

A) Short-term savings | B) Long-term savings | C) Emergency fund | D) Put it on a credit card

Reveal answer & explanation

Correct: C. An unexpected car repair is exactly what the emergency fund exists for. A is reserved for planned goals, such as a trip. B is for retirement or a house — don’t touch it for this. D costs you interest and is what the emergency fund was built to prevent.

5. Why is a high-yield savings account (HYSA) better than a regular bank savings account for your emergency fund?

A) HYSAs are riskier, so they pay more. | B) They offer the same safety but dramatically higher interest, so your money grows faster for free | C) HYSAs don’t allow withdrawals | D) Regular accounts earn more if you have a large balance

Reveal answer & explanation

Correct: B. HYSAs at reputable online banks are FDIC-insured just like regular savings accounts — same protection, but rates of 4–5% vs. 0.01% at many big banks. A is false; the higher rate comes from lower overhead at online banks, not more risk. C is false; you can access your money. D is also false.

Key Takeaways

- Saving provides security, enables goals, reduces stress, and builds wealth.

- Keep three buckets separate: emergency fund, short-term, and long-term savings.

- Compound interest snowballs over time — it earns interest on interest, not just your original amount.

- Starting at 18 vs. 25 can yield ~$480,000 more, even with only $17,000 extra. Time is the variable.

- Park your emergency fund in a high-yield savings account to earn real interest.

- Automate savings and start small if needed — the habit beats the amount.

You know why to save and how compound interest works in a savings context. In Lesson 3.2, we take that logic a step further — into investing, where those same compounding principles can produce even bigger returns over time.

© Coy Academy • Financial Literacy: What School Should’ve Taught About Money