Lesson 1.3: Basic Financial Terminology

Basic Financial Terminology

13 terms that unlock your ability to think, talk, and move with money — no jargon, just plain English.

Every field has its own slang, and money is no different. Once these 13 words click, finance stops feeling like a foreign language. Better yet, you’ll see these exact terms again and again throughout the course. So let’s lock them in now.

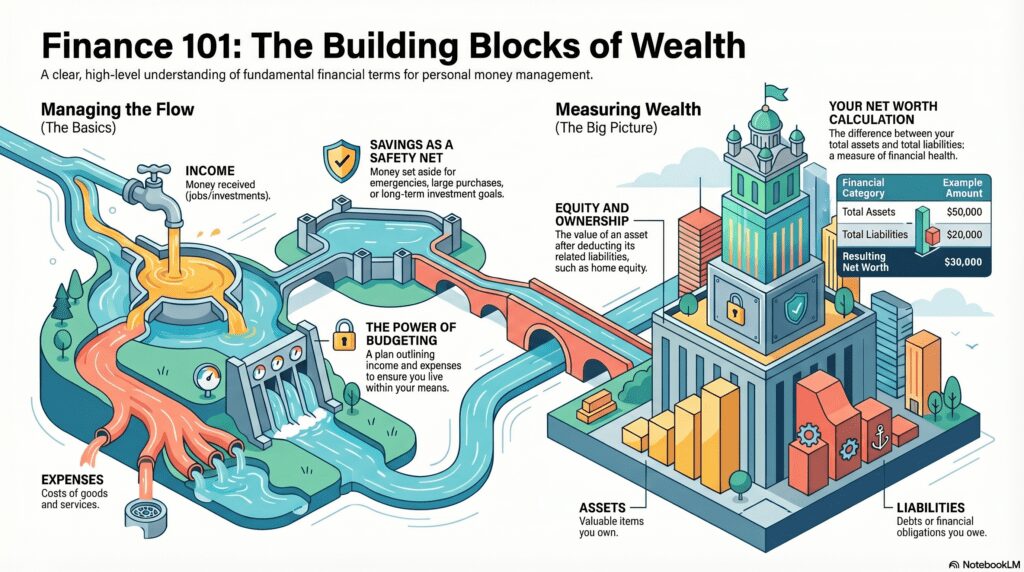

The money you bring in — from a job, a side hustle, or investments. It’s the foundation everything else is built on.

What you spend money on. Some are fixed (same every month) and some are variable (they change).

A plan for your income and expenses over a set time. It keeps you spending on purpose instead of by accident.

Money set aside for later — emergencies, big purchases, or goals. It’s the cushion that keeps surprises from becoming debt.

Money you owe — student loans, credit cards, or that Klarna balance. Some debt is manageable; some is a trap.

Your ability to borrow now and pay back later. Build it well and you unlock lower rates; ignore it and borrowing gets expensive.

The cost of borrowing — or the reward for saving. It can work for you or against you, so know which side you’re on.

Putting money into assets like stocks or funds, expecting it to grow over time. It’s how money makes more money.

Something valuable you own that can grow or earn — cash, investments, property. Assets are the building blocks of wealth.

Something you owe — the flip side of an asset. Liabilities pull your net worth down until they’re paid off.

Your assets minus your liabilities — your personal financial scoreboard. It’s fine if it starts low or even negative; the goal is to grow it.

The slice of an asset you actually own after subtracting what you owe on it. Equity grows as you pay debt down or the asset gains value.

Spreading money across different investments so one bad bet can’t sink you. In short: don’t put it all in one basket.

Check Your Understanding

Pick your answer, then tap “Reveal answer” to see how you did.

1. Maya’s savings account pays her interest, and her credit card charges her interest. In which case is interest working for her?

A) The credit card | B) The savings account | C) Both | D) Neither

Reveal answer & explanation

Correct: B. On savings, interest is the reward the bank pays you. On the credit card, interest is the cost of borrowing — that’s it working against her. So only the savings account pays her.

2. How is net worth calculated?

A) Income − Expenses | B) Assets − Liabilities | C) Savings + Income | D) Credit − Debt

Reveal answer & explanation

Correct: B. Net worth is everything you own minus everything you owe. A describes cash flow, not net worth, and C and D aren’t real formulas.

3. Which of these is a liability?

A) A high-yield savings account | B) An index fund | C) A $1,200 credit card balance | D) Your paycheck

Reveal answer & explanation

Correct: C. A credit card balance is money you owe, so it’s a liability. A and B are assets you own, and D is income.

4. Dumping all your money into a single meme coin is the opposite of which strategy?

A) Budgeting | B) Diversification | C) Saving | D) Net worth

Reveal answer & explanation

Correct: B. Diversification means spreading money across different investments to lower risk. Putting it all in one coin does the exact opposite — one bad move and it’s all gone.

5. Devin pays the same rent every month and spends a different amount on takeout each week. Rent is a ___ expense; takeout is a ___ expense.

A) variable / fixed | B) fixed / variable | C) both fixed | D) both variable

Reveal answer & explanation

Correct: B. Rent stays the same each month, so it’s fixed. Takeout changes week to week, so it’s variable. Knowing the difference makes budgeting way easier.

You now speak the language of money.

These 13 terms show up everywhere from here on out. As you keep going, they’ll shift from vocabulary words into instincts — the way you naturally size up any money decision.

Up next in Lesson 2.1, we’ll look at where money actually comes from — the different sources of income and how to make the most of them.

© Coy Academy • Financial Literacy: What School Should’ve Taught About Money