Lesson 3.3: Understanding Interest and Compounding

Understanding Interest and Compounding

The same force that quietly builds your wealth can quietly bury you in debt — it all depends on which side of it you’re on.

By the end of this lesson, you’ll be able to:

- Explain simple interest and calculate it by hand.

- Explain compound interest, show how it differs from simple interest, and trace it year by year.

- Use the Rule of 72 to estimate how long it takes money to double.

- Describe how compounding frequency (annual vs. monthly) affects growth.

- Explain how compound interest works against you on high-interest debt.

1. What Interest Actually Is

Interest is the price of money over time. When you lend money (to a bank via a savings account, or to a company via a bond), they pay you interest. When you borrow money (a credit card, a loan), you pay interest to the lender. Same concept, opposite position — and the difference between those two positions is everything.

Interest working for you

You put $1,000 in a savings account at 5% annual interest. After one year, you earn $50 without lifting a finger. The bank is the borrower; you are the lender.

Interest working against you

You carry a $1,000 credit card balance at 24% annual interest. After one year, you owe $240 in interest on top of the original $1,000 — and that’s before it compounds.

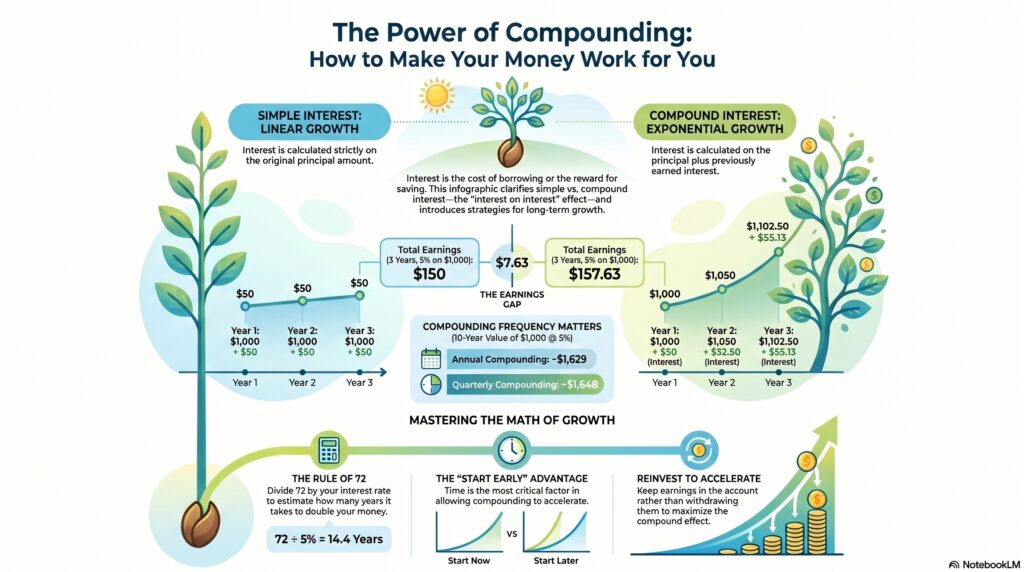

2. Simple Interest: The Baseline

Simple interest is calculated only on the original amount (called the principal). Every period, you earn the same fixed dollar amount. It doesn’t snowball — it just adds a flat payment.

$1,000 × 0.05 × 3 = $150 in interest earned.

Total returned to you: $1,150. Every year, the interest is exactly $50 — no more, no less.

| Year | Interest Earned | Total Balance |

|---|---|---|

| Year 1 | $50 | $1,050 |

| Year 2 | $50 | $1,100 |

| Year 3 | $50 | $1,150 |

Flat and predictable. Same $50 every single year.

3. Compound Interest: When Money Makes Money

Compound interest is calculated on the principal plus all the interest that has already accumulated. Each period, your balance grows, and the next period’s interest is calculated on that larger balance. It snowballs. The longer it runs, the faster it accelerates.

A = $1,000 × (1.05)3 = $1,000 × 1.1576 = $1,157.63

That’s $7.63 more than simple interest — not huge after 3 years, but watch what happens over 30.

The snowball in action: $1,000 at 7% compounded annually

| Year | Interest Earned That Year | Balance |

|---|---|---|

| Year 1 | $70.00 | $1,070 |

| Year 5 | $92.50 | $1,403 |

| Year 10 | $128.80 | $1,967 |

| Year 15 | $179.20 | $2,759 |

| Year 20 | $249.50 | $3,870 |

| Year 25 | $347.20 | $5,427 |

| Year 30 | $483.30 | $7,612 |

You put in $1,000. After 30 years, you have $7,612 — and you’re now earning more in a single year ($483) than your entire original deposit. You added nothing extra. Time and compounding did the rest.

4. Compounding Frequency: How Often It Compounds Matters

Interest can compound annually (once a year), quarterly (4×/year), monthly (12×/year), or even daily. The more frequently it compounds, the more you earn — because you start earning interest on your interest sooner.

| Compounding Frequency | $1,000 at 5% after 10 years |

|---|---|

| Annually (1×/year) | $1,628.89 |

| Quarterly (4×/year) | $1,643.62 |

| Monthly (12×/year) | $1,647.01 |

| Daily (365×/year) | $1,648.72 |

The gap isn’t dramatic at first, but over 30–40 years it adds up. When comparing savings accounts and investment vehicles, look for the APY (Annual Percentage Yield) — it already factors in compounding frequency, making products easy to compare apples-to-apples.

5. The Rule of 72: A Mental Math Shortcut

You don’t need a calculator to estimate how long it takes your money to double. Just use the Rule of 72:

That last one is the gut-punch. A credit card balance at 24% APR doubles in just 3 years if you make no payments. The Rule of 72 works in both directions — and seeing it on debt makes the urgency real.

6. The Dark Side: Compounding Working Against You

Everything that makes compound interest magical for savings makes it brutal for debt. The math doesn’t care which side you’re on — it just runs.

Scenario: $3,000 credit card balance at 24% APR, minimum payments only

The minimum payment is typically 2% of the balance, or $25, whichever is greater.

You spent $3,000. You ended up paying $7,200. Compounding charged you an extra $4,200 — more than the original purchase. This is why the credit card companies love minimum payments. Every month you carry a balance, you’re making compounding work for them.

Pay off high-interest debt first. Every dollar of 24% credit card debt you eliminate is the same as earning a guaranteed 24% return, which no investment can reliably match. Getting out of high-interest debt is investing in yourself.

Check Your Understanding

Pick your answer, then tap “Reveal answer” to check yourself.

1. You invest $2,000 at 5% simple annual interest for 4 years. How much interest do you earn in total?

A) $50 | B) $200 | C) $400 | D) $431

Reveal answer & explanation

Correct: C. Simple Interest = $2,000 × 0.05 × 4 = $400. It’s the same $100 per year, four times. A is just one year at a $1,000 principal. B is the right formula but wrong principal ($1,000, not $2,000). D is the compound interest answer for this scenario — close, but a different calculation.

2. What makes compound interest grow faster than simple interest over time?

A) The interest rate is always higher | B) You earn interest on your accumulated interest, not just the original principal | C) Banks add bonus payments each year | D) It only works in retirement accounts

Reveal answer & explanation

Correct: B. Each period, your balance grows, and the next period’s interest is calculated on that larger number. That snowball effect is the entire engine. A is false — the rate can be identical; the compounding structure is what differs. C and D are both false.

3. Using the Rule of 72, how long does it take $5,000 to double at a 9% annual return?

A) 9 years | B) 8 years | C) 72 years | D) 5 years

Reveal answer & explanation

Correct: B. 72 ÷ 9 = 8 years. The size of the principal ($5,000) doesn’t change the calculation — the Rule of 72 only uses the interest rate. A would be correct at 8% (72 ÷ 8 = 9). C misreads the formula entirely. D would require a rate of 72 ÷ 5 = 14.4%.

4. A savings account compounds monthly, and another compounds annually — both at 5% APR. Which earns more over 10 years?

A) Annual compounding | B) Monthly compounding | C) They are identical | D) It depends on the principal

Reveal answer & explanation

Correct: B. Monthly compounding earns more because interest is added to the balance 12 times a year instead of once, meaning you start earning interest on your interest sooner. From the table: $1,647 (monthly) vs. $1,629 (annually). The gap grows with time. C is a common misconception — same rate doesn’t mean same result.

5. You carry a $3,000 balance on a 24% APR credit card and only make minimum payments. About how long until that balance doubles, using the Rule of 72?

A) 12 years | B) 6 years | C) 3 years | D) 24 years

Reveal answer & explanation

Correct: C. 72 ÷ 24 = 3 years. That $3,000 becomes $6,000 in just 3 years if you’re only making minimum payments. This is exactly why high-interest credit card debt is a financial emergency — compounding is working against you at full speed. A would be a 6% rate. B would be 12%. D misreads the formula entirely.

Key Takeaways

- Simple interest pays a flat amount each period on the principal only — predictable but limited.

- Compound interest earns on the principal and all accumulated interest — it snowballs the longer it runs.

- More frequent compounding = more growth. Look for APY when comparing accounts.

- Rule of 72: Divide 72 by the interest rate to find how many years until money doubles.

- Compounding works in reverse on debt — a 24% credit card balance doubles in 3 years on minimum payments.

- Paying off high-interest debt is the equivalent of a guaranteed high return. Do it first.

Compounding is only one factor in how investments grow. In Lesson 3.4, we look at the other side of the equation — fees and commissions, which compound against you just as relentlessly as interest compounds for you.

© Coy Academy • Financial Literacy: What School Should’ve Taught About Money