Lesson 3.4: Understanding Fees and Commissions

Understanding Fees and Commissions

A 1% fee sounds harmless. Over 30 years it can silently cost you more than $150,000. Here’s how.

By the end of this lesson, you’ll be able to:

- Explain what an expense ratio is and why it’s the fee that matters most.

- Show in real dollars how a high ER compounds against you over decades.

- Identify other common investment fees: load fees, trading commissions, and advisory fees.

- Know what numbers to look for when evaluating a fund.

- Apply a simple rule: when returns are equal, the lower-fee fund always wins.

1. Why Fees Are a Bigger Deal Than They Look

Most people focus entirely on returns — what did the fund earn? But fees are the part of the equation you control. You can’t guarantee a 7% return. You absolutely can choose a fund that charges 0.03% instead of 1%. And over decades, that choice compounds just as relentlessly as interest does — except it’s compounding against you.

Financial educator and author Tony Robbins popularized this insight for mainstream audiences: most everyday investors have no idea how much of their retirement is quietly consumed by fees. Once you see the math, you can’t unsee it.

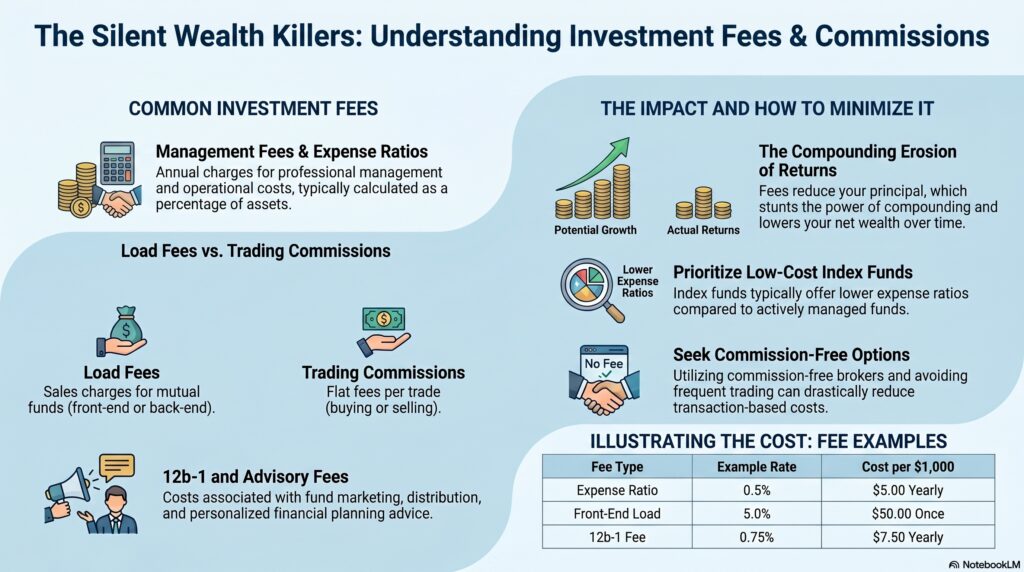

2. The Expense Ratio: The Fee That Matters Most

The expense ratio (ER) is the annual fee every mutual fund and ETF charges to cover its operating costs — management, administration, and marketing. It’s expressed as a percentage of your investment and deducted automatically. You never write a check for it; it’s simply subtracted from your returns before you ever see them.

Example: You invest $10,000 in a fund with a 1% expense ratio. You pay $100 that year. If it earns 7%, you don’t get 7% — you get roughly 6%. Doesn’t sound like much. Now watch what 30 years does to that gap.

The real cost of a 1% fee

Same investor. Same $10,000 starting investment. Same $300/month contribution. Same 7% gross annual return. Only the expense ratio differs.

That $65,000+ difference came from a fee you never directly paid. It was silently deducted each year, which reduced the principal that could compound the following year — and so on for 30 years. The fee didn’t just cost you 1% each year. It cost you the compounding on that 1% every single year after that. This is fee drag, and it’s why the expense ratio is the first number serious investors check.

Illustration assuming 7% gross annual return compounded monthly, $10,000 initial investment, $300/month contributions. Actual results vary.

What’s a good expense ratio?

| Fund Type | Typical ER Range | Verdict |

|---|---|---|

| Index ETFs (Vanguard, Fidelity, Schwab) | 0.03% – 0.20% | Excellent — aim here |

| Actively managed mutual funds | 0.50% – 1.00% | Acceptable only if performance justifies it |

| High-fee or specialty funds | 1.00% – 2.00%+ | Hard to justify — proceed with caution |

Research consistently shows that most actively managed funds don’t beat their benchmark index over the long term — and when you add fees, they fall even further behind.

3. Other Fees Worth Knowing

The ER isn’t the only fee out there. Here are the others you’ll encounter and what to do about each.

A sales commission charged when you buy (front-end load) or sell (back-end load) a mutual fund. Front-end loads of 4–5% mean you start with less money invested from day one.

A marketing and distribution fee buried inside some mutual funds’ expense ratios. You’re paying for the fund to advertise itself to other investors. Up to 1% annually.

Fees charged per trade when buying or selling stocks or ETFs. Most major brokers (Fidelity, Schwab, Robinhood) now offer commission-free stock and ETF trades.

What you pay a financial advisor to manage your money. Often 0.5–1% of assets annually. On a $200,000 portfolio that’s $1,000–$2,000 per year — every year, compounding.

Some brokerages charge annual or monthly fees just to keep the account open. Usually waived if you maintain a minimum balance or have regular activity.

Penalties for pulling money out of certain funds or retirement accounts before a set period. Retirement account early withdrawals can trigger both a penalty and income taxes.

4. How to Check a Fund’s Fees in 60 Seconds

You don’t need to read a 40-page prospectus. Here’s the quick lookup:

When two funds offer similar exposure to the same market, the one with the lower expense ratio will almost always produce the better long-term result. Fees are a guaranteed drag. Returns are not guaranteed. Minimize the thing you can control.

Check Your Understanding

Pick your answer, then tap “Reveal answer” to check yourself.

1. What is an expense ratio?

A) The profit a fund makes each year | B) A one-time fee when you open an account | C) The annual fee a fund charges as a percentage of your investment to cover operating costs | D) The commission your broker earns per trade

Reveal answer & explanation

Correct: C. The expense ratio is charged annually as a percentage of your balance and automatically deducted from returns. A is the opposite — an ER reduces profit to the investor. B describes an account fee. D describes a trading commission, which is a separate type of fee.

2. Why does a 1% expense ratio cost you far more than just 1% of your returns each year?

A) Fees increase with inflation | B) The fee reduces your compounding base, so you lose the compounding on the fee amount every year after | C) Funds charge 1% plus additional hidden fees | D) The government taxes fees at a higher rate

Reveal answer & explanation

Correct: B. Every dollar taken in fees is a dollar that can no longer compound. Over 30 years, you don’t just lose 1% per year — you lose the compounding on that 1%, which is how a modest-sounding fee turns into tens of thousands of dollars of lost wealth. A, C, and D are all false.

3. You’re comparing two S&P 500 index funds. Fund A has an ER of 0.04%; Fund B has an ER of 0.90%. Both track the same index. Which should you pick and why?

A) Fund B, because higher fees mean better management | B) Fund A, because lower fees mean more of your returns stay invested and compound | C) Either is fine since they track the same index | D) Fund B, because it’s more diversified

Reveal answer & explanation

Correct: B. When two funds track the same index, the returns before fees are nearly identical. The lower-ER fund gives you more of those returns. A is the “you get what you pay for” misconception — research shows most higher-fee active funds underperform their benchmark. C ignores that the fee difference compounds dramatically. D is false — diversification is determined by the index, not the ER.

4. A mutual fund charges a 5% front-end load. You invest $2,000. How much is actually working for you in the market from day one?

A) $2,000 | B) $1,950 | C) $1,900 | D) $1,800

Reveal answer & explanation

Correct: C. 5% of $2,000 = $100 in load fees. $2,000 − $100 = $1,900 actually invested. You’re already down 5% before the fund does anything. That’s why no-load funds are generally preferred — 100% of your money starts working immediately. A ignores the load. B and D use the wrong percentages.

5. You find a fund with an expense ratio of 1.5%. Based on what you’ve learned, what should your reaction be?

A) Great — higher ER means more professional management | B) Neutral — ERs don’t affect long-term returns much | C) Cautious — 1.5% is significantly above average and requires a strong performance track record to justify | D) Invest immediately because fees protect against losses

Reveal answer & explanation

Correct: C. A 1.5% ER is well above the industry average for broad-market funds. That fee compounds against you year after year and research shows most high-fee active funds still underperform passive alternatives over long periods. Caution is warranted. A and D are false. B is the exact misconception this lesson exists to correct.

Key Takeaways

- The expense ratio is the most important fee — it’s deducted automatically, compounds against you, and is entirely in your control.

- A 1% ER on a 30-year investment can cost $65,000+ compared to a 0.03% alternative at the same return.

- Target ERs under 0.20% for index funds and ETFs. Most excellent options are under 0.10%.

- Avoid load fees (use no-load funds), excess 12b-1 fees, and advisory fees that aren’t clearly justified.

- When two funds track the same index, the lower-ER fund wins — every time, over time.

- Check fees in 60 seconds: ticker + “expense ratio” on Morningstar or ETF.com. Make it a habit.

You now know what to invest in and how much fees cost you. In Lesson 3.5 we tackle a question a lot of Gen Z investors face first: what’s the difference between investing and trading — and why does it matter which one you’re doing?

© Coy Academy • Financial Literacy: What School Should’ve Taught About Money