Lesson 3.2: Introduction to Investing

Introduction to Investing

Saving keeps your money safe. Investing puts it to work — and that’s a very different thing.

By the end of this lesson, you’ll be able to:

- Explain what investing is and why it differs from saving.

- Name the core investment types and what makes each one distinct.

- Read a risk/return spectrum and place investments on it.

- Understand why risk tolerance and time horizon matter before you invest a dollar.

- Know the right starting point for a first-time investor.

1. Saving vs. Investing: What’s the Difference?

Both saving and investing build wealth — but they do it differently, at different speeds, and for different purposes. Knowing which one to use when is half the battle.

Saving

- Money sits in a bank account earning modest interest.

- Very low risk — FDIC insured up to $250,000.

- Best for: emergency fund, short-term goals, money you may need soon.

- Growth is slow but predictable.

Investing

- Money goes into assets that can grow in value over time.

- Higher potential return — but also real risk of loss.

- Best for: long-term goals like retirement, wealth building.

- Growth can dramatically outpace inflation over decades.

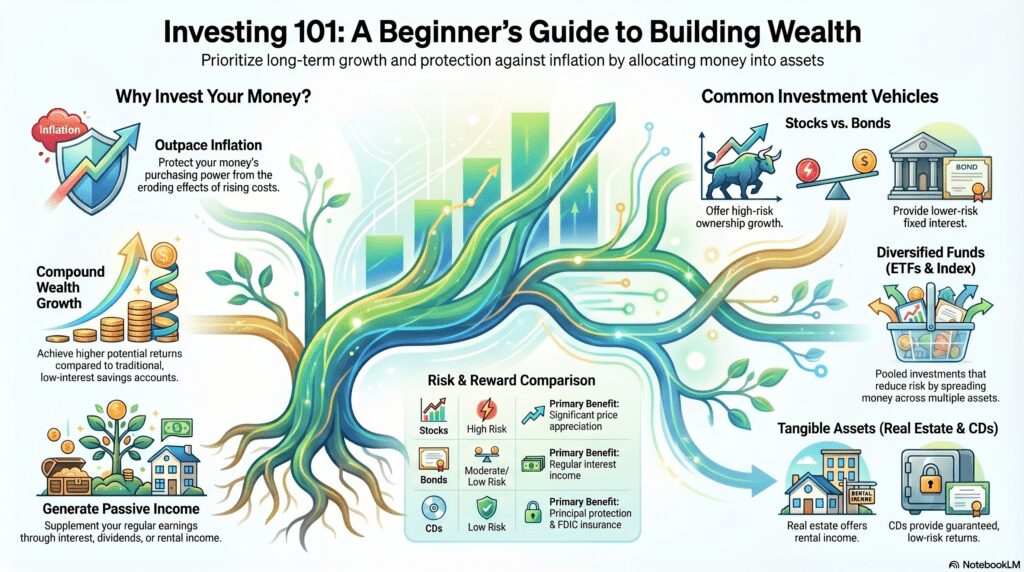

2. Why Investing Matters for You Specifically

There’s one reason investing is especially urgent for Gen Z: inflation. If prices rise 3% a year and your money earns 0.5% in a savings account, your money is quietly losing purchasing power every year. Investing is how you stay ahead of that.

Historically, the stock market has averaged 7–10% annually over long periods. That outpaces inflation by a wide margin.

Dividends and gains can create income streams that don’t require you to trade your time for money.

A house, early retirement, financial independence — none of it happens on a savings-account rate of return alone.

Investment gains compound just like interest does — at potentially much higher rates over time.

3. The Main Investment Types

You don’t need to master all of these right now. What matters is understanding what each one is so you can make sense of conversations about them.

Stocks

A slice of ownership in a company. If the company grows, your slice is worth more. If it tanks, so does your investment.

Bonds

You lend money to a government or company and they pay you back with interest over time. Stable but slow-growing.

Index Funds & ETFs

Baskets of many stocks that track a market index (like the S&P 500). Instant diversification at low cost. The most recommended starting point for beginners.

Mutual Funds

A pooled investment managed by professionals. Diversified like index funds, but actively managed — which usually means higher fees. More on fees in Lesson 3.4.

Real Estate

Buying property to rent out or sell at a profit. High barrier to entry but can generate steady passive income. REITs let you invest in real estate without owning property directly.

Cryptocurrency

Digital currency like Bitcoin or Ethereum. Extremely volatile — can soar or collapse in days. High speculative risk. We cover this fully in Lesson 3.6.

4. The Risk/Return Spectrum

There is no free lunch in investing. Higher potential return always comes with higher risk. The spectrum below shows where the main investment types sit. Understanding this is the single most important concept before you invest anything.

Higher Risk / Higher Return

5. Two Questions Before You Invest Anything

Before picking an investment, answer these two questions honestly. They determine everything else.

What’s my time horizon?

How long before you need this money back? The longer the timeline, the more risk you can take — because markets dip, but historically they recover and grow over long periods.

What’s my risk tolerance?

Could you watch $1,000 drop to $600 without panic-selling? Or would you pull out the moment it dips? Your honest answer shapes which investments fit you.

6. Where Should a First-Time Investor Start?

With so many options, it’s easy to freeze up and do nothing. Here’s the clearest starting path for most young investors:

The beginner’s playbook

Check Your Understanding

Pick your answer, then tap “Reveal answer” to check yourself.

1. What is the main difference between saving and investing?

A) Saving is only for emergencies; investing is for fun | B) Saving preserves money at low risk; investing grows money at higher potential return but with real risk of loss | C) Investing is safer than saving | D) There is no meaningful difference

Reveal answer & explanation

Correct: B. Saving keeps your money protected and accessible; investing puts it into assets that can grow significantly but can also lose value. A misdefines saving. C is the opposite of the truth — investing always carries more risk. D ignores everything that makes them work differently.

2. On the risk/return spectrum, where do index funds sit compared to individual stocks and bonds?

A) Lower risk than bonds | B) Higher risk than individual stocks | C) Between bonds (lower risk) and individual stocks (higher risk) | D) Exactly the same risk as crypto

Reveal answer & explanation

Correct: C. Index funds sit in the medium range — more potential return than bonds, but less concentrated risk than picking individual stocks because they spread across hundreds of companies. A, B, and D all misread the spectrum.

3. Why does a longer time horizon allow for more investment risk?

A) You have more money to lose | B) Markets are less volatile over longer periods | C) You have more years for the market to recover from downturns before you need the money | D) Risk decreases automatically with age

Reveal answer & explanation

Correct: C. Markets dip regularly, but historically recover and grow over long periods. If you have 30 years before you need the money, a temporary 30% drop is just a blip — not a crisis. If you need the money in 2 years, that same drop is catastrophic. B is a misconception; short-term volatility doesn’t disappear, it just matters less over longer timelines.

4. Why is an index fund a commonly recommended starting point for new investors?

A) It guarantees positive returns | B) It focuses all your money on one high-performing stock | C) It gives instant diversification across many companies at low cost | D) It’s only available in retirement accounts

Reveal answer & explanation

Correct: C. An index fund spreads your money across hundreds of companies automatically, so no single company failure sinks you — and the fees are low. A is false; no investment guarantees returns. B is the opposite of diversification. D is false; index funds are available in regular brokerage accounts too.

5. According to the beginner’s playbook, what should you do before investing a single dollar?

A) Open a crypto account | B) Research individual stocks | C) Build at least a $1,000 emergency fund | D) Wait until you earn at least $50,000 a year

Reveal answer & explanation

Correct: C. Investing without an emergency fund is risky because any unexpected expense forces you to sell investments — possibly at a loss — just to cover the bill. The emergency fund protects your investments by keeping them untouched. A and B skip a crucial foundation step. D is a myth — you can start investing with small amounts at any income level.

Key Takeaways

- Saving protects money; investing grows it — use both for different goals and timelines.

- Investing beats inflation over long periods in ways a savings account can’t.

- Higher potential return always means higher risk — there are no exceptions.

- Your time horizon and risk tolerance determine which investments fit you.

- Most beginners do well starting with a low-fee index fund inside a tax-advantaged account.

- Emergency fund first — always. Investing money you might need soon is a recipe for selling at the worst moment.

You’ve got the lay of the land. In Lesson 3.3 we go deeper on the engine behind all of this — exactly how interest compounds, how to calculate it, and why it’s the most powerful force in personal finance.

© Coy Academy • Financial Literacy: What School Should’ve Taught About Money