Lesson 4.1: Defining Assets and Liabilities

Defining Assets and Liabilities

One sentence can change how you see every financial decision you’ll ever make. This lesson is built around it.

By the end of this lesson, you’ll be able to:

- Define assets and liabilities using the framework that actually changes behavior.

- Explain why a car and a personal home are usually liabilities, not assets.

- Identify which assets actually generate income and prioritize acquiring them.

- Understand the nuanced case where a home can become an asset.

- Apply the asset/liability test to any purchase before you make it.

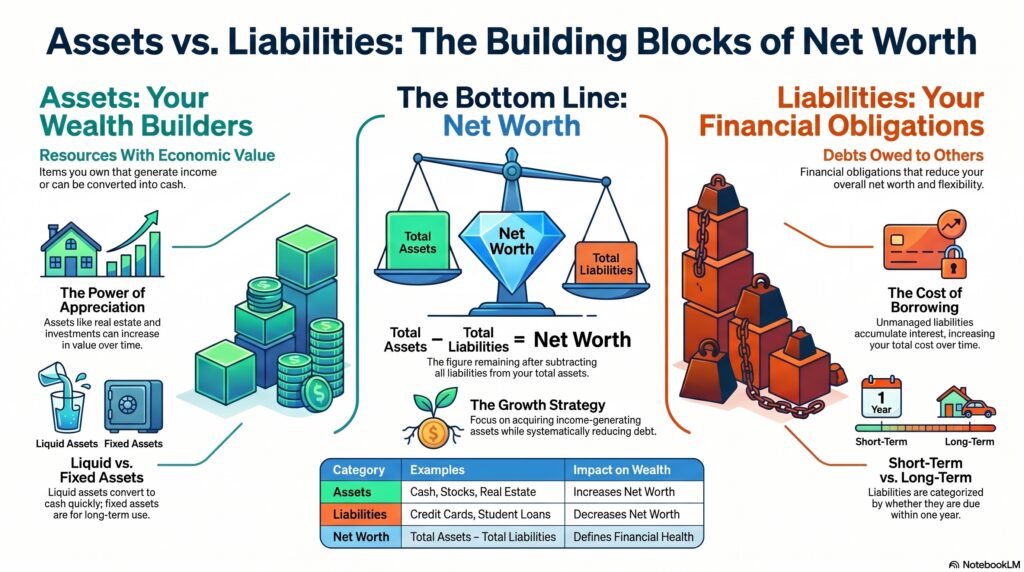

1. The Definition That Changes Everything

Most finance textbooks define assets as “things you own” and liabilities as “things you owe.” That’s technically accurate — and almost completely useless for making real decisions.

Robert Kiyosaki’s Rich Dad Poor Dad introduced a simpler, more powerful definition that cuts through the noise:

into your pocket.

out of your pocket.

That’s it. Read those again. Now apply it to everything you own and everything you’re thinking of buying. The results are often uncomfortable — and exactly right.

The goal of building wealth, then, is straightforward in principle: acquire things that put money in your pocket. Minimize things that take money out. The wealthy do this consistently. Most people do the opposite — they buy liabilities and call them assets.

2. The Expensive Car Is Not an Asset

This one tends to land hard. A car feels like ownership. It’s yours. You have the title. But run it through the test:

The real monthly cost of a $35,000 car

That’s $12,876 a year leaving your pocket. And the car itself is depreciating — losing roughly 15–20% of its value in year one, and continuing to drop every year after. Nothing about this puts money into your pocket. By Kiyosaki’s definition, the car is a liability. A necessary one for many people — but a liability.

The exception: If you use the car to generate income — Uber, DoorDash, mobile business — the portion used for income generation shifts toward an asset. But the personal-use portion is still a liability.

3. “My House Is My Biggest Investment” — Is It?

This is the belief that Kiyosaki challenged most forcefully in Rich Dad Poor Dad — and the one most people push back on hardest. So let’s be precise about it.

The conventional wisdom says: buy a house, it appreciates, it builds equity, it’s your biggest asset. That can be true. But for most primary residences, run the numbers honestly first:

What a $350,000 home actually costs over 30 years

Figures are illustrative estimates. Taxes, insurance, and maintenance vary significantly by location and property. Does not include closing costs, HOA fees, or renovation costs.

Now, has the home also appreciated? Probably. Historically, U.S. home values have risen roughly 3–4% annually, barely ahead of inflation. A $350,000 home with 3% annual appreciation over 30 years might be worth around $850,000. That sounds like a gain of $500,000 — until you remember you spent over a million dollars to own it.

The nuanced truth about homeownership

This doesn’t mean buying a home is wrong. It means being honest about what it is. A primary residence is:

- A forced savings mechanism — equity builds as you pay down the mortgage, which is better than paying rent with nothing to show for it.

- A lifestyle choice — stability, roots, customization. These have real value even if they’re not financial returns.

- Potentially an asset — if you rent part of it out, house hack, or eventually sell in a strong market with meaningful equity.

- Usually a liability on paper — in the Kiyosaki sense, because month after month it takes money out of your pocket in taxes, insurance, interest, and maintenance.

When a home IS an asset

- Rental property — a home generating rent income that exceeds its carrying costs (mortgage + taxes + insurance + maintenance) is a cash-flowing asset by any definition.

- House hacking — buying a duplex or multi-unit, living in one unit, and renting the others. Tenants pay your mortgage while you build equity.

- Short-term rentals — renting out a room or the whole home on platforms like Airbnb when you’re away, generating income from a space you already own.

4. The Assets Worth Prioritizing

If the goal is to build wealth, the move is to direct money toward assets that generate income — assets that put money into your pocket regardless of whether you show up. These are the building blocks of financial independence.

Stocks & Index Funds

Ownership in businesses that earn profit and grow over time. Dividends pay you to hold. Index funds do this at minimal cost across hundreds of companies.

Rental Property

Real estate that generates monthly rent income above carrying costs. Tenants cover your mortgage while you build equity and collect cash flow.

Bonds & CDs

You lend money at a fixed interest rate. Predictable, lower-risk income. Not exciting, but reliably puts money in your pocket on a schedule.

A Business That Runs Without You

Recall the Cashflow Quadrant from 2.1: a real business (B) generates income through systems, not just your hours. Digital products, online courses, and franchises can do this.

Intellectual Property

A book, course, song, app, or patent you create once that continues earning royalties. High upfront effort, but the asset keeps working after you stop.

High-Yield Savings & Money Market

Your parked cash earning 4–5% in an HYSA. Not dramatic, but it’s liquid, safe, and working. Every dollar sitting in a 0.01% account is a dollar not in your pocket.

5. The Asset/Liability Test

Before any significant purchase, ask yourself two questions:

Status spending — the expensive car, the luxury apartment, the designer gear — is one of the primary reasons people with high incomes stay broke. Money flows out fast when every raise goes into looking successful rather than building it.

This doesn’t mean you can never buy a nice car or a home you love. It means doing it with full awareness of what it is: a lifestyle choice that costs money, funded only after your income-generating assets are funded first.

Asset or liability? Run the test:

| Item | Money in or out? | Verdict |

|---|---|---|

| Index fund shares | Dividends + appreciation in | Asset ✓ |

| Personal car (loan + insurance + gas) | $1,000+/mo out | Liability ✗ |

| Rental property (positive cash flow) | Rent income in | Asset ✓ |

| Primary home (mortgage + taxes + maintenance) | Monthly costs out | Usually liability* |

| Credit card balance | Interest charges out | Liability ✗ |

| Online course / book you created | Royalties in | Asset ✓ |

| Student loan | Interest payments out | Liability ✗ |

| High-yield savings account | Interest in | Asset ✓ |

*Can become an asset if it generates income through renting, house hacking, or eventual profitable sale above total cost of ownership.

Check Your Understanding

Pick your answer, then tap “Reveal answer” to check yourself.

1. Using Kiyosaki’s definition, what is an asset?

A) Anything you legally own | B) Something that puts money into your pocket | C) Something that increases in price over time | D) Any physical property you possess

Reveal answer & explanation

Correct: B. Kiyosaki’s definition cuts through accounting language: an asset puts money in your pocket. A is the textbook definition, which would make your car an asset even though it drains money. C isn’t sufficient — a painting might appreciate, but generates no income until sold. D confuses physical ownership with financial function.

2. Why is a personal car considered a liability rather than an asset?

A) Cars don’t belong to you until the loan is paid off | B) It continuously takes money out of your pocket through payments, insurance, gas, and depreciation | C) Cars can’t be sold | D) It’s only a liability if it’s financed

Reveal answer & explanation

Correct: B. A car costs you money every single month and loses value over time — that’s the definition of a liability. A conflates legal ownership with financial classification. C is false. D misses the point — even a paid-off car still costs money for insurance, gas, and maintenance.

3. Under what conditions can a primary home actually function as an asset?

A) When the mortgage is paid off | B) When it generates income — through renting, house hacking, or a profitable sale above total cost of ownership | C) Always — homes always appreciate | D) When it’s in a good school district

Reveal answer & explanation

Correct: B. The moment a home generates income that exceeds its costs, it crosses from liability to asset. House hacking, renting rooms, or Airbnb can do this. A is partially true — a paid-off home has no mortgage but still costs taxes, insurance, and maintenance, so it still takes money out. C ignores that appreciation doesn’t equal profit when total costs are factored in. D has nothing to do with the asset/liability distinction.

4. Someone earns a $10,000 bonus and immediately uses it for a down payment on a luxury car. According to this lesson’s framework, what did they just do?

A) Invested in a depreciating asset | B) Converted a potential asset into a monthly liability | C) Made a smart purchase since the car holds value | D) Built their net worth

Reveal answer & explanation

Correct: B. They took $10,000 that could have purchased income-generating assets and converted it into the down payment on something that will drain money every month going forward. A technically describes what happened but misses the opportunity cost angle. C is false — cars depreciate, they don’t “hold value” reliably. D is incorrect — the car adds a liability, not a net-worth-building asset.

5. Which of these best describes the wealth-building strategy this lesson is built around?

A) Avoid all liabilities at any cost | B) Buy whatever appreciates in value | C) Prioritize acquiring income-generating assets first; fund lifestyle expenses from what remains | D) Pay off all debt before buying any assets

Reveal answer & explanation

Correct: C. The core strategy is asset-first: direct money toward things that put money back in your pocket, and fund lifestyle from the income those assets generate. A is too extreme — some liabilities (a reasonable mortgage, a car you need for work) are part of a real life. B ignores that appreciation without income generation is speculation. D is the Dave Ramsey approach which has merit in high-interest debt scenarios but isn’t the universal rule — investing while paying off low-interest debt can be the smarter math.

Key Takeaways

- Asset = puts money in your pocket. Liability = takes money out. Apply this test before every major purchase.

- A car is a liability. It costs money every month and depreciates. It’s necessary for most people — but it’s not an investment.

- A primary home is usually a liability in the Kiyosaki sense — it costs far more than most people realize over 30 years.

- A home becomes an asset when it generates income: rental, house hacking, or profitable short-term rental.

- Prioritize income-generating assets: index funds, rental property, bonds, businesses, intellectual property.

- Status spending — buying liabilities to look successful — is why high earners often stay broke. Wealth is built by funding assets first.

Now that you can identify an asset, Lesson 4.2 gets into the strategy of actually building wealth through them — how to acquire income-generating assets systematically even on a modest starting income.

© Coy Academy • Financial Literacy: What School Should’ve Taught About Money